Former Fed Chair Ben Bernanke recently asked a question concerning the optimal long-run size of the Fed's balance sheet (Should the Fed keep its balance sheet large?). Bernanke comes down on the side of "keeping the balance sheet close to its current size in the long run." While he does not explicitly say how "size" is defined, I think it's clear he means the size of the balance sheet measured relative to the size of the economy (say, as measured by nominal GDP). According to this measure of size, the Fed would have to grow its balance at the rate of nominal GDP growth.

In addition to the reasons reported by Bernanke, I think there's a public finance argument to be made for keeping the Fed's balance sheet large--at least, under certain conditions--like ensuring that the inflation mandate is met. Let me explain.

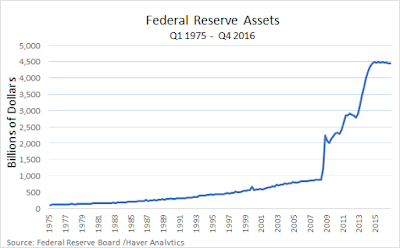

Let's begin with a picture that most people are familiar with.

Prior to 2008, the Fed's balance sheet was under one trillion dollars in size. Prior to 2008, it grew roughly at the same rate as the economy. Most of these assets consisted of short-term U.S. treasury securities. Most of these asset acquisitions were financed with zero-interest money (currency in circulation). Since 2008, the Fed's balance sheet has grown to 4.5 trillion dollars. The composition of assets has moved away from short-term government debt to longer-term debt and mortgage-backed securities. Most of these asset acquisitions were financed with low-interest money (reserves).

Prior to 2008, the Fed's balance sheet was under one trillion dollars in size. Prior to 2008, it grew roughly at the same rate as the economy. Most of these assets consisted of short-term U.S. treasury securities. Most of these asset acquisitions were financed with zero-interest money (currency in circulation). Since 2008, the Fed's balance sheet has grown to 4.5 trillion dollars. The composition of assets has moved away from short-term government debt to longer-term debt and mortgage-backed securities. Most of these asset acquisitions were financed with low-interest money (reserves).

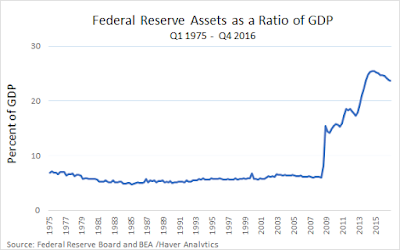

Is 4.5 trillion a big number? Well, yes. But then, the U.S. is a big economy: the U.S. nominal GDP for 2016 is close to 19 trillion dollars. So in measuring the size of the Fed's balance sheet, it probably makes more sense to measure size as a ratio. The following graph plots the size of the Fed's balance sheet as a ratio of nominal GDP.

Prior to 2008, the size of the Fed's balance relative to the economy averaged about 6%. The balance sheet size peaked in 2014 at just over 25%. Note that by this metric, the Fed's balance sheet has been contracting since 2014.

Prior to 2008, the size of the Fed's balance relative to the economy averaged about 6%. The balance sheet size peaked in 2014 at just over 25%. Note that by this metric, the Fed's balance sheet has been contracting since 2014.

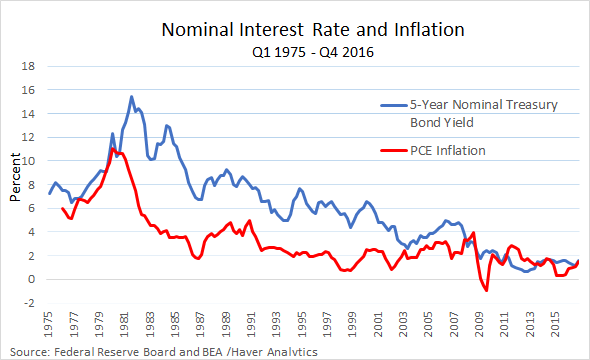

For the record, note that the large expansion in the supply of Fed money was associated with historically low rates of inflation:

Now let's talk about the business of banking. I like to think of a bank as an asset transformer: a bank converts relatively illiquid assets into relatively liquid liabilities. The Fed buys relatively high-yielding (but safe) securities, like U.S. treasury bonds and AAA-rated mortgage-backed securities. It pays for these acquisitions by issuing liabilities (printing money) in the form of low-interest reserves.

Now let's talk about the business of banking. I like to think of a bank as an asset transformer: a bank converts relatively illiquid assets into relatively liquid liabilities. The Fed buys relatively high-yielding (but safe) securities, like U.S. treasury bonds and AAA-rated mortgage-backed securities. It pays for these acquisitions by issuing liabilities (printing money) in the form of low-interest reserves.

The Fed transforms high-interest government debt into low-interest Fed liabilities (money).

The difference between the interest the Fed earns on its assets and the interest it pays on its liabilities is an interest rate spread. Isn't it wonderful to be able to borrow at low rates and invest at high rates? This is precisely what the Fed did with its large scale asset purchase (LSAP) program. Apart from any other effects that this intervention had on the economy, it resulted in huge profits for the Fed. Keep in mind that any profit made by the Fed is remitted to the U.S. Treasury (and thus, ultimately, to the U.S. taxpayer).

So just how much money does the Fed return to the treasury each year? I'm glad you asked, here you go:

In recent years, the Fed has been returning about $80-90 billion per year to the U.S. Treasury. While interest rates were higher in the past, the Fed's balance sheet was much smaller--and so while the profit margin was high, the volume was low. Today the profit margin is smaller, but the balance sheet is much larger. (The distance between the red and blue lines represents the Fed's foregone profit since it started paying interest on reserves in 2008).

In recent years, the Fed has been returning about $80-90 billion per year to the U.S. Treasury. While interest rates were higher in the past, the Fed's balance sheet was much smaller--and so while the profit margin was high, the volume was low. Today the profit margin is smaller, but the balance sheet is much larger. (The distance between the red and blue lines represents the Fed's foregone profit since it started paying interest on reserves in 2008).

What sort of rate of return does the Fed make on its portfolio? The following graph plots Fed payments to the Treasury as a ratio of the Fed's assets.

Since the bulk of the Fed's assets are in the form of U.S. government bonds, it should be no surprise to learn that the rate of return has generally followed the path of market interest rates downward. Still, in recent years, the annual rate of return is about 2%. Given that the Fed is presently financing these assets with cash (0%), ON RRP (0.25%) and IOER (0.50%), the profit margin is still significantly positive (though one wonders about the scope for further policy rate hikes if market rates remain low).

Since the bulk of the Fed's assets are in the form of U.S. government bonds, it should be no surprise to learn that the rate of return has generally followed the path of market interest rates downward. Still, in recent years, the annual rate of return is about 2%. Given that the Fed is presently financing these assets with cash (0%), ON RRP (0.25%) and IOER (0.50%), the profit margin is still significantly positive (though one wonders about the scope for further policy rate hikes if market rates remain low).

In light of this analysis, why are some people calling for the Fed to reduce the size of its balance sheet? Usually the concern is that a large balance sheet portends higher future inflation. But we've been living in a world of lowflation for many years now and we're likely to stay there for the foreseeable future (though central banks should of course remain vigilant!). There is, in fact, some theoretical support for the notion of reducing the Fed's policy rate (subject to the dual mandate and financial stability concerns); see, for example: The Inefficiency of Interest-Bearing National Debt.

Reducing the Fed's balance sheet at this point in time seems like a needless loss for the U.S. taxpayer. Given that the Treasury is marketing a bond, who do you want to hold it? If the debt is held outside the Fed, the government needs some way to pay the 2% carry cost of the debt. The government will in this case have to reduce program spending, increase taxes, or increase the rate of growth of debt-issuance. Alternatively, if the Fed holds the debt, the carry cost is generally much lower. This cost-saving constitutes a net gain for the government. So why not take advantage of it?

***

P.S. I realize there are some who argue that a central bank enables big government. Since the government is too large, we need to end central banking and, in this manner, starve the beast. But this argument amounts to "let's make the government less efficient in terms of financing their operations--that'll force it to get smaller." This line of argument strikes me as naïve--I'm not sure what would prevent the government from simply substituting into different methods of finance. If you want smaller G, then lobby Congress to make G smaller. But given that smaller G, it should still be financed in the most efficient manner possible. And that means following the prescription above.

In addition to the reasons reported by Bernanke, I think there's a public finance argument to be made for keeping the Fed's balance sheet large--at least, under certain conditions--like ensuring that the inflation mandate is met. Let me explain.

Let's begin with a picture that most people are familiar with.

Is 4.5 trillion a big number? Well, yes. But then, the U.S. is a big economy: the U.S. nominal GDP for 2016 is close to 19 trillion dollars. So in measuring the size of the Fed's balance sheet, it probably makes more sense to measure size as a ratio. The following graph plots the size of the Fed's balance sheet as a ratio of nominal GDP.

For the record, note that the large expansion in the supply of Fed money was associated with historically low rates of inflation:

The Fed transforms high-interest government debt into low-interest Fed liabilities (money).

The difference between the interest the Fed earns on its assets and the interest it pays on its liabilities is an interest rate spread. Isn't it wonderful to be able to borrow at low rates and invest at high rates? This is precisely what the Fed did with its large scale asset purchase (LSAP) program. Apart from any other effects that this intervention had on the economy, it resulted in huge profits for the Fed. Keep in mind that any profit made by the Fed is remitted to the U.S. Treasury (and thus, ultimately, to the U.S. taxpayer).

So just how much money does the Fed return to the treasury each year? I'm glad you asked, here you go:

What sort of rate of return does the Fed make on its portfolio? The following graph plots Fed payments to the Treasury as a ratio of the Fed's assets.

In light of this analysis, why are some people calling for the Fed to reduce the size of its balance sheet? Usually the concern is that a large balance sheet portends higher future inflation. But we've been living in a world of lowflation for many years now and we're likely to stay there for the foreseeable future (though central banks should of course remain vigilant!). There is, in fact, some theoretical support for the notion of reducing the Fed's policy rate (subject to the dual mandate and financial stability concerns); see, for example: The Inefficiency of Interest-Bearing National Debt.

Reducing the Fed's balance sheet at this point in time seems like a needless loss for the U.S. taxpayer. Given that the Treasury is marketing a bond, who do you want to hold it? If the debt is held outside the Fed, the government needs some way to pay the 2% carry cost of the debt. The government will in this case have to reduce program spending, increase taxes, or increase the rate of growth of debt-issuance. Alternatively, if the Fed holds the debt, the carry cost is generally much lower. This cost-saving constitutes a net gain for the government. So why not take advantage of it?

***

P.S. I realize there are some who argue that a central bank enables big government. Since the government is too large, we need to end central banking and, in this manner, starve the beast. But this argument amounts to "let's make the government less efficient in terms of financing their operations--that'll force it to get smaller." This line of argument strikes me as naïve--I'm not sure what would prevent the government from simply substituting into different methods of finance. If you want smaller G, then lobby Congress to make G smaller. But given that smaller G, it should still be financed in the most efficient manner possible. And that means following the prescription above.

The US is indeed able to collect massive seigniorage revenues from the rest of the world. I'm not sure if "efficient" is the right way to describe the way it exploits the network effects of its disproportionate role in the financial system. I'd rather have a global system that works well for all involved, and maximizes world GDP, even if that means a higher cost of borrowing for the US.

ReplyDeleteWe need to think of ways to remove frictions and allocate credit efficiently throughout the world system. Exorbitant privilege seems (to me, at least) fundamentally incompatible with those goals.

Don't hold your breath waiting for U.S. monetary and fiscal policy to operate in the manner you envisage. In any case, the "exorbitant privilege" you speak of was not endowed; it was earned. And no one forces other countries to use USD or UST.

DeleteI agree with Anwer. In my own words...profit is a useful measure of the success of a microeconomic entity like a corporation. In contrast, printing the nation's currency is macro and it's monopolistic. Thus profit does not tell us much.

DeleteDavid,

ReplyDeleteI'm not sure you are framing the balance sheet issue correctly. No reputable bond manager would talk the way you or the Fed does: "There's no issue with my $4.5tr balance sheet, because I've made so much money playing the interest rate spread the past three years."

As Steve Williamson points out, the Fed is no different than any other financial intermediary when it buys risk assets. It has no proprietary information, and is exploiting no market failure. Rather, it is simply betting that short rates will remain below long yields. This is about as garden-variety of a hedge fund strategy as one can imagine. That doesn't mean it is riskless. Clearly, short rates could rise to well exceed current long yields. In an inflationary dynamic, the Fed's failure to predict inflation exposes it to getting behind the curve. In this situation, the real rate fails to rise as the Fed hikes, or it even falls further, stoking yet more inflation. The Fed does have a specific problem: when it loses money, the deficit expands, which fuels inflation further (no different than a tax cut implemented as inflation accelerates -- not a good idea).

Who is on the hook for that duration risk? The taxpayer, through foregone Treasury remittances from seigniorage which are already baked into CBO baseline projections. Any shortfall from that baseline increases their tax liability.

The reason to shrink the Fed's balance sheet is to eliminate taxpayer risk borne by an institution that has absolutely no advantage in taking duration risk on its balance sheet (as you say, the Fed's models are not for predicting...). In fact, the Fed is at a big disadvantage: any hedge fund that telegraphed trillion dollar bond buys would be front-run, and if, to boot, it didn't even pretend to engage in any price discovery, it would have its head handed to them. This is the "hedge fund" that is taking risk on behalf of the taxpayer.

Those are some great observations, Diego. I think David is highlighting the fact that large amounts of seigniorage are available. Why not just go for it? It's bad for the world overall, but the world isn't joining hands to build a better system.

DeleteDiego, you raise a legitimate concern. Here are some thoughts in reply.

DeleteFirst, the duration risk you speak of could be mitigated considerably if the Fed restricted itself to short-duration assets.

Second, even if the Fed had to temporarily raise its policy rate above the yield on its portfolio, the net present value to the U.S. taxpayer is still likely to remain positive (in my mind) since any such events are rare, and there are more periods in which the spread operates in the Fed's favor.

Third, suppose that the Fed balance sheet was "small" as in pre-2008 (with scarce reserves). Suppose the Fed has to temporarily raise its policy rate, say, in response to an inflation concern. Then the U.S. treasury is the agency bearing the higher interest-cost of debt issuance. That is, the treasury has been speculating that interest rates will remain low. Given this, what difference does in make to the U.S. taxpayer whether it is the Fed or the Treasury that takes the hit of an interest-rate increase?

Thanks for your reply. My responses in order:

ReplyDelete1. If the Fed reduced duration considerably, it would also eliminate whatever impact it thinks it's having on the economy (see S. Williamson's latest).

2. This statement seems to go against finance. Absent arbitrage, any trade faces an ex-ante NPV of zero, with the risk of being on the negative returns tail of the distribution. With QE, the Fed shifts it's balance sheet from pure arbitrage (seigniorage) to a normal bet. You may be arguing there is no opportunity cost to the Fed's capital. This is not correct given the possibility of earning seigniorage.

3. I agree. Outside of seigniorage, it's better to look at the consolidated balance sheet. QE dramatically reduced the duration of gov't liabilities. The next time we have inflation, the deficit will expand as a result, and it will contribute to more inflation. The taxpayer is on the hook for this risk. Why does it matter if the Fed did is responsible for this risk instead of Treasury? Because the Founders gave the power of the purse to the lower house for a reason: voters can hold specific representatives accountable for their votes authorizing Treasury spending. With QE, there is no specific accountability for the Fed's actions, only general.

And my reply to your responses :)

Delete1. Who cares if the balance sheet no longer has the conventional effects? If a one-year UST is yielding anything significantly higher than the interest on Fed liabilities, then the Fed can make a profit for the government.

2. I'm not sure I understand. The Fed has a unique market position: only the Fed can issue Fed liabilities, the ultimate settlement instrument in the economy. This is one reason why Fed liabilities are so highly valued (will be held even at low yield). This advantage can be used to help finance government operations more efficiently. Whether the Fed fully exploits the arbitrage opportunity depends on a host of factors (economic and political).

3. The Fed is surely accountable. The Fed chair and governors are appointed by Congress for limited terms. Fed chair must regular testify in front of Congress. If the public does not like what the Fed is doing, they can lobby their representatives in Congress to modify the Federal Reserve Act, etc.

On 2.: The Fed has no unique powers as an intermediary other than seigniorage (exchanging non-interest bearing reserves for t-bills). If it issues IOR-paying reserves, it acts exactly as Treasury, and there is no spread between T-bills and the IOR

DeleteFor the Fed's balance sheet to add value beyond plain-vanilla seigniorage, there must be some information asymmetry at work. The Fed either needs better predictions than the market; or access to info the market doesn't have; or there needs to be some market failure the Fed can both recognize and exploit (i.e. the LOLR "lemons problem"). In the absence of these, the Fed is, again as Williamson argues, just another financial intermediary.

Even Farmer justifies risk asset purchases under a market failure (sunspots). The problem is he provides no guidance as to how the Fed can recognize such a failure. His advice to the Fed amounts to "buy low and sell high", which, of course, all financial intermediaries aspire to :).

Friedman's Optimum Quantity of Money (modified by allowing the central bank to pay interest on money)?

ReplyDeleteI like Nick's answer. I would like to go all the way and produce a world system that yields satiation, instead of giving so much of the seigniorage to the US.

DeleteThe fundamental issue here is whether the state’s liabilities should take the form of interest yielding so called “debt” or the form of (normally) non-interest yielding base money, or perhaps some mixture of the two. Strikes me that “Fed balance sheet speak” is just an not very useful, if not positively misleading way of considering that question.

ReplyDeleteMilton Friedman argued for the abolition of the “interest yielding stuff”. Warren Mosler ditto. I.e. they both argued that the only liability should be base money. There are good reasons for that, as follows.

First, what’s the point of the state borrowing money when it can print the stuff? There is no point. One impotant reason politicians borrow (as pointed out by David Hume 250 years ago) is to ingratiate themselves with voters – voters are more acutely aware of tax increases than interest rate rises caused by extra borrowing.

Second, conventional fiscal stimulus (i.e. “the state borrows $X, spends $X and gives $X of bonds to lenders) is just barmy. The purpose of that is stimulus, but the effect of borrowing (considered in isolation) is the OPPOSITE: i.e. it’s deflationary. Thus conventional fiscal stimulus makes as much sense as throwing dirt over your car before cleaning it.

The point of borrowing existing money rather than printing new money is that the former method of finance is generally less inflationary.

DeleteI agree that borrowing is less inflationary than printing per $: that’s partially for the reason I gave above, namely that there’s a big deflationary element in the borrowing option, namely the borrowing itself. In other words for a given amount of stimulus (and hence also a given amount of inflation) you need fewer dollars with the “print” option. So the fact that the borrowing option is less inflationary per $ is irrelevant, far as I can see.

DeleteTreasury can get pretty much the same financing kick by issuing short term bills – instead of channelling bonds through the Fed. Yes, there may be a spread between IOR and bills. But it won’t be material longer term in the context of the all in financing cost for Treasury – if short term bills are issued to buyers outside of the central bank instead. What would have been seigniorage becomes a direct reduction in finance cost of a similar magnitude.

ReplyDeleteThat also makes Treasury’s management of its effective financing term structure a little more straightforward and somewhat more under its direct control at all times. Although that’s probably not a big concern in the scenario of a fat Fed balance sheet - provided the size of Fed reserve issuance is also viewed as a minimum level of effective short term financing for Treasury – i.e. Treasury has to be comfortable in not having the option to extend term on that part of its debt portfolio. That is not necessarily without its problems. I think the larger issue lies not so much in the nature of the Fed balance sheet, but in the implications for the rest of the world – domestic and foreign. To the degree that there is a big demand for what are viewed as the very best safe assets in the world, domestic and foreign, the “trapping” of effective Treasury financing within the Fed balance sheet reduces the external supply of those safe assets. The rest of the world – domestic and foreign - does not have access to Fed reserves. That’s a minus. And Treasury could avoid this altogether by issuing bills instead of channelling its financing through bank reserves.

And that leads to the question of just how “efficient” proposals for a fat Fed balance sheet are for their effect on the primary customers of the Fed – the commercial banks. The nature of excess reserves is very interesting when you consider the position of the banking system as a whole. Aggregate reserves are in fact not liquid in the sense that the banking system as a whole can’t “sell” that position to non-banks. This is actually a weird type of restriction on the management of liquidity. And this is where a large excess reserve position runs the risk of becoming dysfunctional – or “inefficient” to use a word you’ve used in another sense. Nevertheless, if the commercial banks are jammed with excess reserves that they don’t actually need for normal settlement purposes, perhaps there is some minimum level of “liquidity” stipulated below which the banks should not drop according to regulatory liquidity assessment. If the Fed is committed to a fat balance sheet for such reasons of broad system liquidity management, then it should set a new type or new increment of required system reserves based on that assessment. E.g. a $ 1 trillion required reserve increment might be specified and then assigned bank by bank according to regulatory capital requirements. The advantage of doing that is that there is less dysfunction among bank reserve managers trying to plot strategy about what should be their notional share of a forced system excess. Otherwise, that sort of individual bank flailing on individual strategies to respond to the eternal presence of a forced system excess is potentially dysfunctional when the system is up and running on a fully healthy basis. It has already been demonstrated that the system can run efficiently - when the banks are relatively healthy – when excess reserves are miniscule in proportion to the scale of US banking. This was proven to be the case for decades prior to the financial crisis. That to me is more in line with the idea of “efficient”. And I would extend that to say that a fat Fed balance sheet is a sloppy Fed balance sheet – unless thoughtfully formalized with a new required reserve structure bank by bank.

...

"Aggregate reserves are in fact not liquid in the sense that the banking system as a whole can’t “sell” that position to non-banks. This is actually a weird type of restriction on the management of liquidity."

DeleteTrue, reserves are used a settlement device (they find their way outside the banking system only when depositors make redemptions for cash). Do you have any thoughts about the desirability of opening up the Fed's balance sheet (access to reserve accounts) to the general public?

I haven’t put much thought into it, but my impression is that the motivation for this type of proposal includes a commingling of several different factors that are not all that coherent when viewed together. Suppose for simplicity that the demand for physical cash today is separable into two different purposes – the regular medium of exchange purpose (although this is probably being eroded over time by electronic forms of money and credit) and the rest (which includes nefarious store of value advantages). I think those consumers who want cash for regular purposes use it, not because it is issued by the central bank, but because of its convenience as a medium of exchange. It wouldn’t matter so much if the same cash was issued by individual commercial banks, assuming creditworthiness of that cash across the system of commercial banks (backed by something similar to deposit insurance perhaps). Similarly, I think those who prefer the convenience of electronic money are mostly comfortable in doing within its existing form as issued by commercial banks. I’m not sure there is a pressing demand for electronic money as issued by the central bank. That said, I guess there will always be Chicago Plan type proposals that favor demand deposit money issued by the central bank, or by some similar effective arrangement that effectively extracts those deposits from the rest of the business of commercial banking. But those proposals are driven by credit quality concerns rather than convenience considerations. They are designed in the context of a big picture banking system risk issue in which the relevant electronic form is a secondary issue. Yet still other proposals favor electronic money issued by the central bank as a displacement for central bank cash, because it would provide a platform for a negative interest rate capability. Again, that is quite a different motivation. So I think a number of things are being commingled in this sort of question. I think the point of all of it is that it would be important to identity quite clearly the problem to be solved or the question to be answered with such proposals, since they cut across questions of both credit quality and electronic convenience.

DeleteI neglected to mention a couple of other motivating issues, including a desired reduction in nefarious uses of currency as a store of value, and a generalized desire to “take advantage of” whatever benefit it is that bitcoin/block-chain is supposed to be bringing to the world at large. I’m quite sceptical of the latter, because I think that this motivation is being shouted out by a lot of people who don’t know much about existing bank payment technology platforms. It is also instructive that the banks themselves are engaged in aggressive research on that front in order to understand it, take any advantage of it, and preclude the outside threat to the system deposit base.

Delete...

ReplyDeleteA couple of other points. People occasionally float the idea that the existing excess reserve position can be used to fund future currency issuance and emerging increments to future required reserve levels under the existing rules. This is a ludicrous line of thought – really silly. It show an utter failure of numerate intelligence on the subject. Williamson mentioned something about this I think, pointing out the same problem. I did a back of the envelope calculation years ago and came up with a similar time frame of about 60 years or something. Silly stuff.

Finally, the academic framework for monetary theory seems to suffer eternally for a lack of distinction between issues of commercial bank liquidity management and commercial bank capital management. Monetary theory drowns in the absence of understanding the nature of bank capital in the balance sheet expansion process. That is what accounts in part for example for misconstruing excess reserves as a source of potential inflation. Banks don’t “use” excess reserves as the rationale for risk lending. Full stop.

This is kinda picked up by others but...

ReplyDelete1) IOER is more expensive than overnight Bills, so better to have the Treasury issue $2 trn or whatever in Bills and deposit that cash at the Fed. It would save taxpayers money.

2) More importantly, term premium is negative on most coupon Treasuries, so ex ante, it is cheaper for the Treasury to issue long-term debt (and by long-term, more like 5-years) than to fund short-term, either through IOER or Bills.

Most of the commentary like the above seems to miss that both the Fed and UST "fund" the government, just through differently structured liabilities (dollar bills are liabilities...) and the US government doesn't face a budget constraint. Why not just force the banking system to hold some egregious amount of required reserves that can only be US government liabilities (and exempt banks from holding capital against them)? Or, like the UK, why not require pension funds to hold ludicrously high amounts of long-term sovereign debt? That's just as good a strategy as any.

Its all a matter of political economy, but the exorbitant privilege strategy is a pretty good one, only problem is we squandered the surplus on providing tax cuts which exacerbated inequality and now we have that yellow-haired vulgarian running our country.

Hi David,

ReplyDelete"If the debt is held outside the Fed, the government needs some way to pay the 2% carry cost of the debt."

Here's another option to keeping the Fed's balance sheet large. Looking at FRED, I see that 1-month treasury bills yield just 0.5%, the same as IOER. If the Fed were to begin shrinking its balance sheet by selling off its bonds (which as you say yield ~2%), the government could in turn buy up and retire those bonds by issuing 1-month t-bills. Whichever route is taken, the tax payer ends up in the same spot. They are either on the hook for paying 0.5% IOER or a 0.5% rate on t-bills.

From a public finance perspective, why doesn't the government replace more long-term & pricey treasury bonds with low-cost treasury bills?

I like John Cochrane's proposal to turn all the federal debt into money. It takes us closer to liquidity satiation.

DeleteLooking through the other comments, I see I'm just saying the same thing as JKH & Anonymous.

DeleteOff topic: I wish to criticize a Fed chart.

ReplyDeleteIt’s this chart which purports to show the change in NAIRU over time.

https://fred.stlouisfed.org/series/NROU

The chart implies that NAIRU can be measured with the same accuracy as the content of other Fed charts: inflation, the money supply and so on. I suggest it is delusional to think NAIRU can be estimated with any great accuracy. Thus the chart should have some sort of “health warning” on it to the effect that the chart simply shows the Fed’s best guess as to what NAIRU is.

Also, I find this sentence just under the chart very odd:

“The natural rate of unemployment (NAIRU) is the rate of unemployment arising from all sources except fluctuations in aggregate demand.” Surely a more normal definition is something like the Wiki definition, namely the “level of unemployment below which inflation rises”. The word “accelerates” would be better than “rises”: the A in NAIRU refers to “accelerate”.

One of the most inaccurate concepts in the whole discussion of the Fed's balance sheet is the myth of a "Fed profit" that gets passed along to the Treasury. This "profit" comes solely from interest on US government securities, so returning the "profit" to the Treasury is taking money from one pocket and putting it in another. There is simply no economic profit to the government from the Fed's portfolio.

ReplyDeleteIn fact what the Fed has done is shorten the US government's debt maturities. While UST wants to lock in low rates by issuing long bonds, the Fed buys long bonds financed with short-term interest on reserves, so the total US government is more exposed to interest rate increases. On top of this, the interest on reserves is about 0.25% above market t-bill rates, so this amounts to an unnecessary and inappropriate subsidy to the commercial banking system currently amounting to $4 billion.

Further, the Fed's balance sheet growth is highly correlated with increased bad debt in the banking system. (Described in my paper at https://ssrn.com/abstract=2733295 .) The Financial Crisis came from excess growth in Fed assets that led to excess growth in bank assets, that resulted in bad debt.

So, what's not to like about the Fed's excessive balance sheet? Just increased interest rate expose to the federal government, excess subsidy spending to banks, and more bad debt.